Australians Pension Age Changes – Retirement planning in Australia is entering a period of major change as updates to the pension age push many people to rethink long-held assumptions about when and how they will stop working. With 2026 approaching, adjustments to eligibility timelines are reshaping financial decisions for individuals approaching old age as well as those still years away from retirement. These changes affect income planning, superannuation drawdowns, and access to government support. For Australians, understanding how the revised pension age works is now essential to avoid gaps in income and ensure long-term financial stability.

Pension Age Changes and Retirement Planning for Australians in 2026

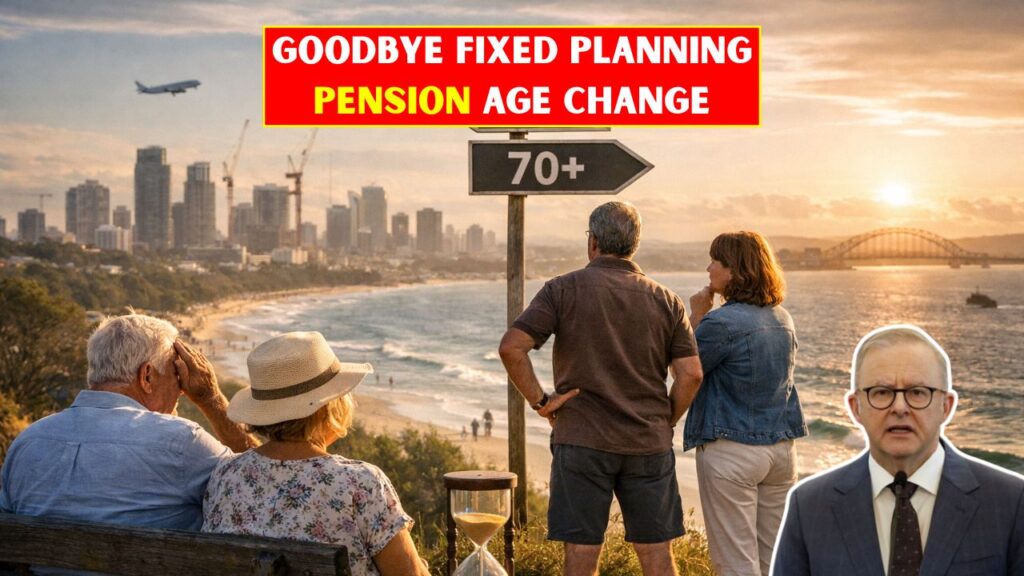

The upcoming pension age changes are prompting Australians to reassess traditional retirement planning models. Under current policy settings, the qualifying age for the Age Pension has been gradually increasing, and by 2026 it will apply uniformly to new claimants. This means individuals who expected to retire earlier may need to rely more heavily on personal savings or superannuation before government support begins. For Australian citizens nearing retirement, the shift alters timelines for income security, healthcare planning, and lifestyle choices. Financial advisers are encouraging people to review their retirement strategies early, factoring in employment flexibility, part-time work options, and revised savings goals to align with the new pension age reality.

Driving Licence Rules Change in Australia with New Renewal Tests and Fees Starting in 2026

Driving Licence Rules Change in Australia with New Renewal Tests and Fees Starting in 2026

How Australia’s Updated Pension Eligibility Impacts Future Retirees

Across Australia, the revised pension eligibility rules are influencing how future retirees approach long-term financial decisions. Those born after specific cutoff dates will reach pension eligibility later than previous generations, extending the period between workforce exit and pension access. This change has particular implications for individuals in physically demanding jobs or those with limited superannuation balances. The Australian retirement system still combines superannuation, private savings, and the Age Pension, but the balance between these elements is shifting. As eligibility ages rise, planning for income continuity becomes more critical, especially for older individuals who may face health or employment challenges before reaching pension age.

Australia Activates Air Traffic Cameras Nationwide as Drivers Face Instant Fines Up to $1,500

Australia Activates Air Traffic Cameras Nationwide as Drivers Face Instant Fines Up to $1,500

| Category | Key Information |

|---|---|

| Standard Pension Age | 67 years for eligible recipients |

| Applies From | Fully in effect by 2026 |

| Who Is Affected | Australians born after the set transition dates |

| Income Support Gap | May rely on superannuation or savings before pension |

| Planning Action | Review retirement income strategy early |

Rethinking Retirement Timelines Under Canberra Government Pension Rules

The Canberra government’s approach to pension age reform reflects longer life expectancy and sustainability goals, but it also requires Australians to rethink retirement timelines. Many people are now planning to remain in the workforce longer, either full-time or in flexible roles, to bridge the gap until pension eligibility. This shift can have benefits, such as higher superannuation balances and continued engagement, but it also demands realistic planning. Individuals must consider health, job availability, and skill relevance as they extend working lives. Adapting to these pension rules means retirement is becoming a more gradual transition rather than a fixed endpoint.

Financial Preparation for Australian Citizens Facing Later Pension Access

For Australian citizens, preparing financially for later pension access involves more than simply delaying retirement. It requires reassessing superannuation contributions, investment strategies, and expected living costs during the years before pension eligibility. Many are choosing to boost voluntary super contributions earlier in their careers to offset the later start of government payments. Others are exploring diversified income sources, such as part-time work or phased retirement options. Clear understanding of pension rules helps individuals avoid financial stress and make informed decisions that support a stable and comfortable retirement despite the changing age requirements.

Frequently Asked Questions (FAQs)

1. What is the pension age in Australia from 2026?

The pension age will be 67 years for eligible Australians from 2026 onward.

2. Who will be affected by the pension age changes?

Individuals born after the transition dates who have not yet reached pension eligibility will be affected.

3. Can Australians retire earlier than the pension age?

Yes, but they may need to rely on superannuation or personal savings before accessing the Age Pension.

4. Should retirement plans be updated due to these changes?

Yes, reviewing retirement and income plans early is recommended to align with the new pension age rules.